pSivida (PSDV) has been on stockmatusow's radar for over one year now, as we first wrote about the company in April of 2012 detailing the company's good long term prospects. When it comes to small cap companies, the first thing we look for is strong leadership. Dr. Paul Ashton, pSivida's CEO certainly fits the bill as an honest and straight-forward leader. For our first article, I had the pleasure of interviewing Dr. Ashton and was impressed with his straight-forward no-nonsense talk.

I always say "bet on the jockey, not the horse," and in pSvidia's case, I feel both the jockey and the horse have very strong potential.

Not only does Dr. Ashton handle the company's finances very well while operating on a small budget, he has also created and developed three of the only four products approved by either the US or EU for the long-term, sustained-release delivery of drugs to treat chronic eye disease.

The only criticism I have of Dr. Ashton is that he might be a bit too conservative in his approach, and is not the most "exciting" speaker in terms of delivering company presentations in conferences and earnings calls. However, I would prefer to have a CEO act in this manner rather than over-guiding and making "pie in the sky" promises, which is almost always a sign of poor management. In my opinion, Dr. Ashton is an honest man with good character -- something investors should take solace in.

- Product Pipeline

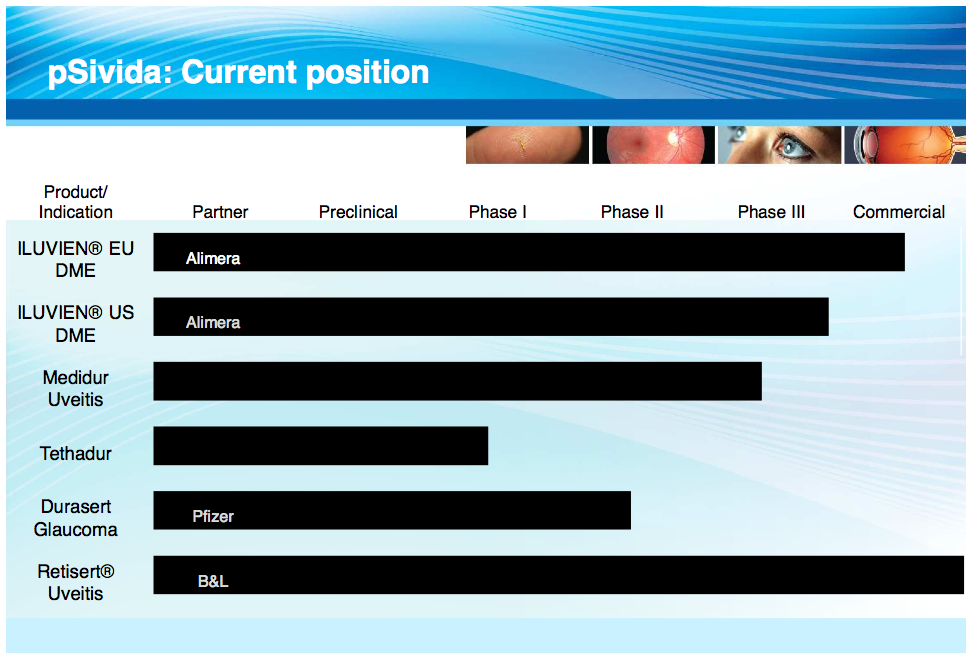

pSivida specializes in treatments for eye conditions. The company's products address issues with glaucoma, posterior uveitis, and diabetic macular edema (DME). ILUVIEN is being developed to treat DME, Medidur to treat uveitis, and Durasert for glaucoma. Tethadur may be the company's most valuable technology platform because it has the potential to deliver peptides, proteins, and antibodies with a better safety and efficacy profile than other options.

In 2012, the global ophthalmic drugs market reached $18.7B, and is expected to continue growing.

The age-related macular degeneration (AMD) and diabetic retinopathy segment of that market generated just over $3 billion in 2010. Visiongain projects those revenues to climb to nearly $5.1 billion by 2014 while ten-year forecasts for ocular disease therapeutics predict steady growth.

According to Dr. Ashton,

Back-of-the-eye diseases are the leading cause of blindness in the developed world, but they're very difficult to treat. The challenge is delivering drugs to the back of the eye.

There have been big advances in wet AMD therapies recently, targeting vascular endothelial growth factor (VEGF). Excessive VEGF production causes blood vessels to become fragile, allowing fluids to leak into surrounding tissues where they may damage the macula and create blind spots in central vision.

Eye drops have been a standard delivery mechanism, but they don't penetrate to the back of the eye. GlaxoSmithKline (GSK) and Sanofi (SNY) are developing penetrating eye drops, which could have profound implications for glaucoma simply because people forget to administer eye drops, especially for conditions that aren't painful. Therefore, physicians never know for certain if the drugs are ineffective or whether the patient is non-compliant.

Standard therapy has been Genentech's (Genentech is a member of the Roche Group (RHHBY) ) VEGF inhibitors Lucentis (ranibizumab) and the off-label use of Avastin® (bevacizumab). These are equally effective at improving vision, but the improvement only lasts six to eight weeks.

GlaxoSmithKline has two drugs in clinical trials for ocular therapy: darapladib, an oral Lp-PLA2 inhibitor for diabetic macular edema, and pazopanib (Votrient®), a multi-kinase angiogenesis inhibitor in eye drop form for AMD. Early-stage work also is under way for neovascular AMD, dry AMD, diabetic retinopathy, diabetic macula edema, uveitis, and glaucoma, as well as for technologies for drug delivery.

Implants offer another approach. pSivida just developed an implant that can be injected in a physician's office, using a fine-gauge needle to place an eyelash-sized tube at the back of the eye. The injectable micro-inserts already are approved to treat chronic diabetic macular edema in several European countries. The micro-inserts release a therapeutic at a consistent rate during 36 months, delivering the compound directly to the eye and thereby avoiding systemic side effects. In the U.S., the first patient was enrolled in June in Phase III trials to study their use in treating posterior uveitis. That condition is the third leading cause of blindness in the U.S., affecting approximately 175,000 people. Other applications also are possible.

Tethadur could be pSivida's most valuable technology, with its potential to deliver proteins, peptides, and other small molecules. This technology is a drug delivery system that relies on nanostructuring to achieve optimal delivery. It can be used alone or in combination with pSivida's other technologies.

Unlike most polymer-based drug delivery systems, the manufacture of Tethadur does not require complex chemistry and the final product is pure silicon irrespective of the delivery characteristics imparted by the nanostructuring process.

Tethadur distinguishes itself from other delivery systems by its heat and radiation stability, simplifying the manufacturing and sterilization process.

pSivida's Durasert Technology is a miniaturized, injectable, sustained-release drug delivery system designed to advance the treatment of medical conditions in critical areas, such as ophthalmology.

- Bioerodible or non-erodible

- Administered in an office visit

- Linear sustained-release kinetics (days/weeks/months/years)

- Injectable via needles as small as 25-guage

- Highly efficient/drug loading (up to 80%)

Pfizer Inc. (PFE) has the option to license Duraset from pSivda if they so choose to do so. It's worth noting that Pfizer also owns about 10% stock in pSivida, so its in its best interest that Duraset is successful. In our opinion, Pfizer might acquire pSivida if Duraset proves to be successful. We believe this could occur sometime in 2014/early 2015 as pSivida moves further along in the development of its Duraset technology.

- ILUVIEN catalyst

ILUVIEN is a small injectable implant developed with partner Alimera (ALIM) to treat diabetic macular edema. DME is a condition where the blood vessels in the retina leak into the macula, causing blurry central vision. If left untreated, patients can experience severe blurriness or even blindness. Currently, patients get a procedure called laser photocoagulation, which essentially seals the leaky blood vessels. Although this procedure corrects the patient's problems with leaky blood vessels, patients also experience trouble with night vision.

The drug treatment is currently approved in the European Union (EU), which is projected to have $140M to $400M in sales. There are about one million patients in the EU and pSivida is set to receive 20% of those profits. pSivida has already received $30M in royalty payments from Alimera and has the potential to receive $25M more upon United States approval.

Alimera and pSivida have been working on getting ILUVIEN approved in the United States, where there are an additional one million patients with DME. The companies have received Complete Response LetterS (CRL) from the FDA for ILUVIEN on December 23, 2010, November 11, 2011, and again on October 17, 2013.

In a recent press release filing by both companies it stated:

Identifying concerns regarding the benefit to risk and safety profiles of ILUVIEN, the FDA stated that the NDA could not be approved in its present form. To address the clinical and statistical deficiencies identified, the FDA indicated that results from a new clinical trial would need to be submitted, together with at least 12 months of follow-up for all enrolled patients. The FDA suggested that a meeting with the Dermatologic and Ophthalmic Drugs Advisory Committee may be of assistance in addressing the deficiencies identified above and providing advice whether a patient population can be identified in which the benefits of the drug product might outweigh the risks. Alimera reported that in a separate written communication from the staff of the FDA, it was notified that an Advisory Committee meeting would be convened on January 27, 2014. In the CRL, the FDA also referenced deficiencies at the facility where ILUVIEN is manufactured.

What is intriguing about this situation is that the FDA granted pSivida and Alimera an Advisory Committee (ADCOM) meeting on January 27, 2014. It is extremely rare for a company to receive a CRL and then have an ADCOM a few months later. This shows that the FDA is willing to work with the companies in getting ILUVIEN approved.

Approval from the FDA is important for pSivida because it would give the company more funds to leverage its proprietary pipeline. Also, the FDA would allow data from ILUVIEN trials to be used in the development of Medidur. This would significantly improve the financial standing of the pSivida and leave the company incredibly undervalued after the CRL news.

Additionally, we have heard some buzz that indicates that pSivida has interest from many institutions, and that a share offering to raise cash would be supported and may be forthcoming. This would be a huge positive for the company, as additional liquidity in the stock would allow for more institutional support, which could lead to a much higher stock price along with more analyst coverage moving forward.

With a market cap under $90M, we feel pSivida is hugely undervalued/under speculated in the current sector. Additionally, a well-supported public offering with prior institutional commitment would be very beneficial and lead us to buy any such offering.

| Share Statistics | |

| Avg Vol (3 month): | 568,978 |

| Avg Vol (10 day): | 109,983 |

| Shares Outstanding: | 26.96M |

| Float: | 22.64M |

| % Held by Insiders: | 30.85% |

| % Held by Institutions: | 12.60% |

| Shares Short (as of Oct 31, 2013): | 1.25M |

| Short Ratio (as of Oct 31, 2013): | 1.10 |

| Short % of Float (as of Oct 31, 2013): | 4.80% |

| Shares Short (prior month): | 949.03K |

An additional raise of let's say about 7M shares would definitely be a positive for the company and the stock in this case. Many raises are engaged in by small cap biotechs because the companies are running low on cash. This is not the case with pSivida. In this case, as mentioned, an offering would allow more institutional support.

Key points why pSivida has a legit shot to become a larger cap company over time:

- Opthalmology is a big area of interest as the population ages; take into account the success of Lucentis, which was developed by Genentech and is marketed in the United States by Genentech and elsewhere by Novartis (NVS). Also Regeneron's (REGN) eElea are having great success.

- Technologies that are for ophthalmology now are adaptable for other parts of the body. (there is currently an evaluation agreement with the Hospital for Special Surgery in NYC for example, and their focus is orthopaedics). The uveitis program and the bioerodible version of the underlying technology of Iluvien for glaucoma with Pfizer.

- In 2012, the global ophthalmic drugs market reached $18.7B, and is expected to continue growing. With pSivida advancing new technology in this segment, considering the large market space here, even a small grab of this market would indicate pSivida to obtain a market cap well over $500M or more in the years to come.

- Strong CEO who manages money well, delivers honest and straight-forward guidance, and who has created almost all of pSivida's technology.

- Conclusion

If pSivida engages in a successful offering which attracts institutions, the company could end up being a great small cap investment. The company's strong management and undervalued pipeline are added bonuses. Dr. Ashton not only manages money well on a small budget, he has also created the company's current pipeline. Dr. Ashton is a strong manager, just the kind of leadership we look for in small cap developmental biotechs. pSivida's long term chances at success are very high in our opinion, and a gain of 200% to 300% over the next year or two seems very reasonable to us.

Ophthalmology, especially wet and dry AMD and DME is a fast growing and lucrative market. Dr. Ashton is an excellent money manager who cares about shareholders and works on a modest budget.

We feel a great long term award is in store here for those who demonstrate patience, should persevere.

Disclosure: Team Matusow is long PSDV.

Disclaimer: This article is intended for informational and entertainment use only, and should not be construed as professional investment advice. They are my opinions only. Trading stocks is risky -- always be sure to know and understand your risk tolerance. You can incur substantial financial losses in any trade or investment. Always do your own due diligence before buying and selling any stock, and/or consult with a licensed financial adviser.

")