Updated 6/22: Cleaned up thesis to include that we feel the stock price will tank hard even if Afrezza is approved.

- Background and Story of Afreza

MannKind Corporation (MNKD) is a biopharmaceutical company that focuses on the discovery, development, and commercialization of therapeutic products for diabetes and cancer in the United States, Europe, and Asia. Its' lead product candidate is Afrezza Inhalation Powder, a rapid-acting mealtime insulin therapy for the treatment of adult patients with Type 1 and Type 2 diabetes mellitus for the control of hyperglycemia.

Because of its unique pharmacokinetic profile, Afrezza may be a promising new therapy for patients with Type 1 and Type 2 diabetes, as it controls post meal-time glucose levels with less weight gain and lower risk of hypoglycemia.

Afrezza received its first Complete Response Letter (CRL) from the FDA in March of 2010. A CRL is what the FDA responds with when the organization decides not to approve a drug for marketing and distribution. From Mannkind’s Website regarding the first CRL:

“The Complete Response letter related to the AFREZZA application requested several items, including information and currently available clinical data that support the clinical utility of AFREZZA and information about the comparability of the commercial version of the MedTone inhaler to the earlier version of this device that was used in pivotal clinical trials. The letter cited no safety concerns, but requested updated safety data related to AFREZZA. The letter also requested changes to the proposed labeling of the cartridges, foil pouches and cartons.

The letter did not require any additional pre-marketing clinical studies in order for the FDA to complete its review of the NDA.

As recommended by the FDA, MannKind will request an End-of-Review meeting with the agency to discuss its approach for resolving the remaining issues.”

Now, let’s look at the second CRL the company received and issued a press release on about a year later:

“The principal issue raised by the FDA concerned the usage of in vitro performance data and clinical pharmacology data to bridge MannKind’s next-generation inhaler to the phase III trials conducted using its MedTone inhaler. The FDA has requested that MannKind conduct two clinical trials with the next-generation inhaler (type 1/type 2 diabetes). The FDA has also requested additional information concerning the performance characteristics, usage, handling, shipment and storage of the next-generation device, an update of safety information related to AFREZZA as well as information on proposed user training and changes to the proposed labeling of the device, blister pack, foil wrap and cartons.”

Again, the FDA is concerned with Afrezzza’s potential safety issues that could be attached with insulin inhalation., namely cancer risks that could be associated with Afrezza.

The Adcom recommended a post approval safety trial, but for reasons I will mention below, it’s more likely pre clinical data will be required since it appears Mannkind has offered no pre clinical studies on potential cancer risks. In fact, when considering Mannkind's constant mis guidance and misleading activities for which they have been successfully sued over in the past, we believe Mannkind does not have this data. This presents a huge potential problem for the FDA, and something the adcom ignored, much as another adcom (see below) ignored solid data when rejecting to recommend a certain drug (Zohydro) for approval, of which the FDA went against and rightly approved the drug anyways.

In other words, while adcom might think it's approvable now, I believe the FDA will not follow adcom here as it did not follow on the Zohydro adcom. (more on that later on)

Additionally, I believe the FDA does not want another Exubera type issue on its' hands

In this regard, Mannkind has seemed to ignore the FDA two times now, which is very typical of this company -- to have an aloof attitude towards the FDA.

In the Type 1 diabetes study, insulin levels were significantly higher in the Afrezza arm compared to the control arm. The FDA raised concerns here about the background basal insulin levels that were significantly higher in the Afrezza arm compared to the control arm.

In the Type 2 study, the FDA said that Afrezza was superior to placebo for the primary endpoint of HbA1c reduction, but it also pointed out comparative effectiveness data showing how Afrezza was inferior to just about all currently available type 2 diabetes therapies.

The above factor goes in part to show that Afrezza is not quite an unmet need, but rather an "unmet want" as there are equal and superior treatments for diabetics on the market now. Afrezza can be considered a very small unmet need for patients who simply cannot receive injectable insulin. When I think of a true unmet need, I think of Acadia's (ACAD) Pimavanserin.

Even if it’s approved, no big pharma will partner with Mannkind for Afrezza. The best Mannkind can hope for royalty deal, and that is my independent opinion. My sources tell me the same thing. Simply stated, Afrezza does not have the blockbuster potential that its' management (with its' history of misleading statements) and its' "Jim Jones" like cult followers claim and believe.

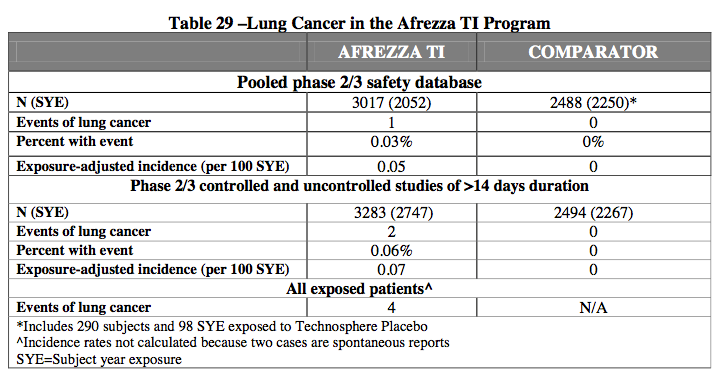

The FDA also raised concerns about Afrezza’s lung safety, including a small, but higher incidence of lung cancer seen in Afrezza patients which both CRL excerpts that Mannkind press released seems to be pointing towards with "an update on safety information for Afrezza"

So what we have here is a drug with potential safety issues that has shown marginal efficacy. The FDA looks at this to make its decision on whether or not to approve a drug. The Adcom believed the benefits outweigh the risks. I believe the Adcom got this wrong and based their decision more on emotion and personal views. We saw something similar in another adcom which I will mention below.

- Concerns from Afrezza data

Some of our concerns with Afrezza are: lung safety issues, dropout rates, missing data, and lower efficacy when compared to subcutaneous insulin. Additionally, some believe that if the missing data and/or dropout data were included, the Phase III efficacy would have failed. The dropout rate for Afrezza was higher than Novolog and many patients dropped out due to the lack of efficacy.

In the Adcom, MNKD really stressed Hb1ac control. In trials it did show a benefit, but some speculate it may have been due to a less efficacious drug.

Given all that, the Adcom participants voted YES on approval. However, almost all voting members stated all these concerns attached. Most agreed that if approved, it would only be used for a strict subset of patients and a safety trial should be conducted.

The question is whether the FDA would take the risk of approving such a device/drug without CLEAR efficacy data and more importantly CLEAR safety data. I think a CRL could definitely be justified, given the lack of clarity and the patient size population that would be effected. Given the history with Exubera, it wouldn't surprise me if they gave another CRL.

However, even if it is approved, I would suspect very very tight label restrictions that would severely limit commercial success. They have no partner likely because big pharma knows that even if approved it won't be a success given these restrictions.

- Atypical dose response relationship: In some studies increasing doses of Afrezza did not increase glucose lowering effect.

- In trial 171, Afrezza was shown to provide statistically inferior HbA1c reduction compared to aspart in patients with type 1 diabetes but the upper 85% confidence interval around the difference in effect between arms remained within the pre-specified non-inferiority margin of .4%. Factors identified in the reviews susceptible to affecting reliability of the estimate included baseline HbA1c that did not fully reflect inpact of run-in phase, differential dropout rates and missing data, as well as inadequate optimization of insulins in the control arm.

- Dosing regiment that was tested in the Phase III trials is different from that Mannkind submitted for the new label.

The FDA will consider the above factors along with a potentially more pertinent issue, the manufacturing process. This is something Adcom’s have no influence on, and something both traders and investors are for some reason are not considering here.

The FDA will consider the above factors along with a potentially more pertinent issue, the manufacturing process. This is something Adcom’s have no influence on, and something both traders and investors are for some reason are not considering here.

- We Think Afrezza Will Likely be Rejected Again For Several Reasons, the Most Prevalent Being the Manufacturing Process

In the second CRL the FDA issued Mannkind, the principal issue raised by the FDA concerned the usage of in vitro performance data and clinical pharmacology data to bridge MannKind’s next-generation inhaler to the phase III trials conducted using its MedTone inhaler. As mentioned, the FDA requested that MannKind conduct two additional clinical trials with the next-generation, with at least one trial including a treatment group using the MedTone inhaler in order to obtain a head-to-head comparison of the data for the two devices. In the complete response letter, the FDA stated that after an adequate titration of study medication there should be at least twelve weeks of relatively stable insulin dosing at the end of the treatment period.

The above guidance from the FDA “appears” to have been met by Mann, and Adcom has input on this factor, but was it actually met?

Phase III trials typically involve a thousand patients or more. In the main Phase III study comparing Afrezza to Novolog, only 175 patients were on the drug using MannKind’s next generation inhaler. In this, we feel once again that Mannkind has taken an aloof attitude towards the FDA and is trying to "shortcut" its's way towards approval.

We also think it’s possible the Adcom received outside pressure and put personal bias over professional sense to vote on recommending Afrezza, basically equating to the inverse of not recommending Zogenic’s (ZGNX) Zohydro by a wide margin of 11–2 against. The FDA went against that particular Adcom for Zohydro and approved the drug anyways.

The Zohydro adcom panel seemed to vote on personal bias when it soundly rejected to recommend Zohydro for approval. That adcom reasoned that Zohydro could be abused by patients, rather than ruling on the specific questions whether it was safe and effective in the recommended dosage, which the FDA decided against that adcom that Zohydro is.

With Afrezza, it seems adcom was more caught up in being part of making history by recommending Afrezza for approval, while strangely remarking they recognized the safety issues, with a few of the adcom members choosing to add a scale of 1 to 10 on the confidence of their yes vote -- most remarked that their confidence level was a 2.

As mentioned above, the FDA has also requested additional information concerning the performance characteristics, usage, handling, shipment and storage of the device, an update of safety information related to AFREZZA as well as information on proposed user training and changes to the proposed labeling of the device, blister pack, foil wrap and cartons– for the second time, which it appears Mannkind is ignoring as it’s typical of it to do.

Additionally, adcom does not have input on the manufacturing process, which is specialized on and completed at Mannkind’s own custom plant, built in 2008.

Also of note, Mannkind made the following admissions recently on a Wells Fargo conference call:

- There will be label restrictions if approved.

- Based on current commercial capacity, Mannkind can only serve up to 370,000 patients a year

- Mannkind is comfortable with there cash position up to approval. (Absurd view, Mannkind constantly raises money, is in big debt, and will need more money, so we can reasonably conclude it will need to raise money to sell and manufacture Afrezza if approved.)

- Expects REMS

- Expects a 10 year post approval study if Afrezza is approved.

From above, we can see why big pharma has no interest in partnering with Mannkind if Afrezza gains FDA approval next month, but may have interest in a small royalty deal. Big pharma will not take on the risk of potential safety issues with Afrezza for the reward of marketing this product to a small and restricted subset of patients. In other words, in spite of what self deceived Mannkind Cult followers claim, Afrezza is likely to be a flop commercially, just as $DNDN's provenge, which that stock was "pumped" all the way up to absurd valuations, had cult followers thinking Provenge was a blockbuster, etc, etc. Sound minded investors who use reason over emotional greed factors know the real deal with Afrezza. (Also think of $AMRN's Vascepa.)

Mannkind has continually mislead investors on this front. In fact, (read further down) Mannkind was successfully sued for "misleading statements" that inflated their stock price.

- Mannkind Still Has Job Openings for Key Positions in Manufacturing Plant

With less than 1 month to go before the scheduled FDA approval decision date of July 15th, 2014, Mannkind still lists several job openings at this plant:

We think this does not bode well for Mannkind, especially if we look at its history of dismissing specific guidance the FDA asked for before the last two CRL’s. It’s late in the game here for Mannkind with Afrezza tio still have unfilled important jobs, so again we think Mannkind is ill prepared in this regard.

It’s worth noting that in March 2013, Mannkind’s manufacturing expenses were $9.3M, compared to a current expense of a little over $1M. This hardly seems to us that manufacturing is ramping up and ready for approval.

- Rejection on manufacturing could result in studies being required pre-approval

Adcom does not give input on the manufacturing process of a drug and/or device. Although Adcom did recommend approval based on benefits outweighing current safety concerns, it also recommended post approval safety studies to be conducted.

Here lies the issue that most traders and investors are missing – if a CRL is issued for Afrezza’s unique and complicated manufacturing process. This could mean asking for the Adcom recommended safety study while the company attempts to correct manufacturing issues. It will take a minimum of six months to correct any such manufacturing issues, and likely longer because of the specialized nature of the Afrezza manufacturing process. Investors just aren't considering this, and seem to be over exuberant on Afrezza's approval chances.

We think this will bite Mannkind and cause a 3rd CRL, which will both mention manufacturing and may require an additional safety study before Mannkind can submit a new NDA. We believe with Mannkind’s poor financial position, debt, convertible notes, and other factors, the stock price is likely to plummet to under $2 a share if rejected, and the company will likely engage in even more dilution with even more misleading statements. Why am I so harsh on Mannkind in the regard? Because it has a documented history of misleading investors.

- Examples of FDA Rejecting Adcom Recommendations – Generally Rare, But Still Happen

Zogenics’ Drug Zohydro (as mentioned earlier) received an 11 to 2 vote against recommending the pure opiod pain killer back in December of 2012. At the time, the FDA panel member did remark it could still be approved with restrictions. In October 2013, Zohydro was in fact approved by the FDA with a Risk Evaluation and Mitigation Strategies (REMS) designation.

The FDA representive at Zogenics Adcom remarked that Zohydro could be approved with restrictions. At Afrezza Adcom, the FDA representive remarked that the efficacy appears marginal and had safety concerns. Investors need to take careful note of this.

- Examples of Mannkinds’s continued Misguidance Concerning Partnerships and Settled Lawsuit over Stock Manipulation

Before Afrezza received its second CRL in 2011, Mann was telling investors that he saw no warning signs from the FDA indicating Afrezza approval would be derailed and he noted other companies were interested in partnering for a new product launch. This is typical from Mann, which shows his complete lack of understanding how the FDA applies regulations. Al has been promising investors for years that a partnership with a big pharma is in the works.

My sources tell me that big pharma is only interested in a royalty deal, which would not help Mannkind much, if at all to get it out of debt. These sources feel big companies have zero interest in offering a real partnership deal, as in a 50/50, 60/40, 70/30, or even 80/20. Simply speaking, Afrezza really is not an huge money unmet need, (more like an unmet want) and would only be prescribed to a smaller amount of diabetics. As remarked by several panel member sat adcom, traditional insulin is still clearly better and more efficacious than Afrezza.

Patients might certainly want a more convenient and fast acting form of insulin here, but we do not see this as a true unmet need and neither does big pharma — the efficacy and safety profile just isn’t superior in any way, with the possible exception being for the type 2 diabetic indication.

Big Pharma was burned with Exubera, another insulin inhaler.They thought that Exubera would be a huge money maker, and it wasn't. In fact, it was a flop.

So, it’s not likely they want to revisit a similar product again in terms of risking big dollars. With a standard royalty deal, Afrezza may be able to bring in $100 to $200 a year, which Mannkind would receive $10M to $20M in revenues based on the probability of a severe label restriction that would only be lifted once, and if ever, Mannkind provides long term safety data on Afrezza. This equates to a market cap of no more than $200M dollars, at best $400m. With the fully diluted share count around 400M, this equates to $0.50 to $1 a share.

This is hardly the billions of dollars that retail investors have been constantly expecting and wrongly believing will happen to support the current hugely inflated market cap of over $5B and hardly enough money to pay off the huge amount of debt it has racked up in order to get Afrezza approved - if approved at all.

Additionally, company COO Edstrom stated that in 6-8 weeks, Mannkind will have a partner for Afrezza. This comment was made on June 12, 2014. Another company insider commented that Edstrom could be wrong, but did not issue any retraction.

No truly responsible management would give such a specific guidance like this, especially one who does things correctly, ever! It’s irresponsible as good management never makes promises and gives specific assurance to investors on a factor such as partnerships which is really an unknown variable.Mannkind has been engaging in this foolish behavior for years as The Street's lead biotech writer Adam Feuerstein clearly documents.

There is never any guarantee in business, and especially a guarantee that assures investors a partnership is imminent. Good companies would keep such information private and among insiders if it was actually close to a real partnership. The evidence is clear on this view as Mannkind has now been promising such a partner for the better part of 10 years.

Also worth noting are the constant “positive” articles concerning Mannkind. Rarely do a company’s prospects work out with so much positive sentiment out there without a real contrarian view, which we believe will prove to be the correct one when all is said and done.

It’s very critical to note that in 2012, a lawsuit against MannKind Corporation was settled in favor of the plantiff, alleging that MannKind’s stock price was artificially inflated as a result of untrue or materially misleading statements related to MannKind’s communications with the FDA about Afrezza -- how Mannkind represented this communication to the market at large.

Subsequently, a $23 million securities class action settlement was awarded to shareholders who claimed the pharmaceutical company misled them about the regulatory approval prospects of its diabetes drug Afrezza, allegedly causing up to $158 million in investor losses. The judge in the case ruled;

“The proposed settlement requires MannKind to implement corporate governance reforms, including the establishment of a board-level disclosure committee, amendments to the board’s audit committee charter and revisions to the qualifications for director independence.”

Mannkind appears to be continuing in the same behavior for which it was sued for before by making a bold claim that it will have a partner for Afrezza in 6 to 8 weeks.

We feel very strongly that a promise of having a partner for Afrezza secured within 6 to 8 weeks after potential approval is irresponsible at best, and potentially misleading as no company can make such a promise to investors with a statement of such specific expectation. The correct and ethical way to relate to its’ investor base would have been to say, “we are hopeful that in 6 to 8 weeks we will secure a partner for Afrezza.”

- Convertible Note Holders Have a Self -Interest in Making Money from Stock Sales

Mannkind is a mess of debt via convertible notes, which one example among many can be found here. Deerfield, who as of recently hasn’t enjoyed a stellar reputation, has paid out a ton of cash to Mannkind in exchange for a lot of notes which can be converted to shares when the stock is above a certain price range, as it is currently.

Deerfield was one of 23 firms fined the by SEC for stock manipulation when it improperly participated in public stock offerings after selling short those same stocks. Such violations typically result in illicit profits for the firms involved in the scheme.

Basically, what Deerfield was being fined here for is that it acted improperly in advance of a secondary public offering, and/or offerings.

One example of how a finance company can manipulate a stock is that it will short sell a stock to knock the price way down, churn to cover the shares while going long, then initiate a mass short covering. This squeezes other shorts and attracts momentum and speculative traders to pump the stock price way up.

Then the financiers sell their longs, and shortly thereafter, massively sell short. Soon afterwards, a public offering is announced, which tanks the stock. The financiers then cover their shorts and make huge profits. Many finance companies make money both long and short this way, which is illegal. Additionally, this is typical with small cap companies, especially small cap biotechs.

This same technique can be used to inflate a stock for convertible note holders to convert those notes, then sell at the inflated prices to make a ton of cash.

- Conclusion

Mannkind has shown it has irresponsible management and has been sued and settled out of court for engaging in misleading statements to investors. The company has continually misguided and misinformed the market, has made promises of a large partnership deal for years now to no avail, and has specifically guided that a major partnership within 6 to 8 weeks from now is to be expected -- same as the years of doing exactly this, but no partner has signed on to date for the better part of 10 years, which is failed guidance at best.

Afrezza has shown some marginal benefits, especially with type 2 diabetes, but safety questions remain. If the FDA approves Afrezza and someone dies or becomes seriously ill as a direct result of using the product, the organization will have a nightmare on its hands. The risk/reward in approving Afrezza just is not there in our opinion because we strongly feel that it's not a true money making unmet need, but rather as we mention before, an unmet want with only a very small subset of patients based on current data, could be considered an unmet need. Afrezza, even if approved will not be a significant money maker, and that is what the market really cares about when push comes to shove.

All of this does not take into consideration what we believe will be a CRL first and foremost on the manufacturing process, and potentially because of high patient drop out rate, the low amount of trial participants, and potential cancer risks which are all unknowns.

Mannkind still has key jobs open for its manufacturing plant, which indicates to us that the company might not properly planning for approval. The FDA issues CRL’s for manufacturing quite often for minor infractions (many want to see this changed). We have to wonder how many FDA infractions Mannkind has in its plant, especially with key positions being left unfilled, and in lieu of 2 CRL’s that seems to ask Mannkind to address this. Why did the FDA have to ask a second time in the second CRL?

Alfred Mann has also constantly misguided, and has achieved a strange cult leader like status. “Mannkindians” (what I call them) have even made YouTube videos praising Al Mann and Mannkind, while bashing on the likes of Adam Feuerstein simply because he takes a contrarian view as we do – lunacy!

Don’t get us wrong, we definitely want to see diabetics get good treatment, but we also want to safe and truly innovative products marketed by good companies with good management. A great part of this safety is ensuring that Afrezza is in fact safe to use for the long term, does not cause certain forms of cancer, and is manufactured safely and consistently, with proper labeling and instructions.

Mannkind has shown to engage in questionable management at best, having been sued and settled with an investor class over the claim of inflated stock prices from misleading statements, along with a history of not following FDA guidance, and failed guidance concerning potential partnerships. The COO is offering guidance that a partner will sign on within 6 to 8 weeks after assumed approval, which we feel is more of the same misleading statements for which Mannkind has been successfully sued over before in the past. It seems to us that the spots on a leopard never change. The past actions of management tell us a great deal of what to expect in the future. This is how an a stout investor make decisions, and not on an emotional bias which includes ignorance of such factors.

Therefore, we predict that at the very least Afrezza is approved with severe label restrictions, will be required to engage in at least a 10 year study, which will tank the stock price to near $2 a share in short period of time.

We are more inclined to believe that Afrezza will receive a 3rd CRL, with the main issues being missing patient data and potential cancer risks. along with problems in the manufacturing process. Subsequently, we believe as the result of this, the FDA will ask Mannkind to either engage a good sized trial on potential safety issues with Afrezza pre approval, or require more pre clinical data on potential cancer risks, or both.

Also, it’s possible the FDA requests a trial that demonstrates that patients know how to use the device properly if Mannkind has not yet provided such data to the FDA, of which the organization has asked Mannkind before in 2 consecutive CRL’s as per Mannkind’s own press released excerpts from the CRL's.

The adcom did not ask for the same data the FDA has, and issued a recommendation on a limited set of data it had before it, and we think it made the wrong decision, in the inverted same that the Zohydro adcom made a wrong decision there.

It also seems to us that the adcom bowed to public pressure along with using emotion over logic, also similar to how the Zohydro Adcom did by voting against that drug which the FDA ended up approving.

Adcoms gives guidance whether a drug is approvable in its current form. Adcom believes Afrezza is. For all the reasons mentioned, we believe it isn’t – time will tell.

")

Matt retracted the 6 to 8 weeks comment by the COO today. I am really worried about the fact that MNKD hasn’t found an Associate Director of Maintenance! That is quite a find Scott! Did you stop to think it will be months under the best of circumstances before they can start manufacturing? I would think they could find someone to fill those high profile positions you mention such as janitor by then.

Yes, because he took heat for it — proves our point that Mannkind has irresponsible management which shows they cannot be trusted. This trust goes directly into if they have actually followed FDA guidance which they have shown they have not done in the past.

If you think a Manufacturing operator is simply a janitor, perhaps you should consider something else besides investing? There are other jobs we did not list, because of a copy/paste error. I will update those shortly.

If they are not ready now to manufacture, they will get a CRL. Do you understand that the FDA requires manufacturing to be online and ready to go before they will issue an approval?

So, yes i did think about your statement, and it bolsters my viewpoint! Thanks for the comments, keep em coming!

So, yes i did think about your statement, and it bolsters my viewpoint! Thanks for the comments, keep em coming!

Hello Scott, thx for the article. Interesting.

I have a question if you don’t mind. You mention that MNKD is having issues with their factory in danbury yet when I review the inspections performed by the FDA at that facility I noticed that out of 3 inspections done (twice in 2009 and once in 2013) they had been issued NAI’s (no issues). What specifically are you referencing when speaking to factory issues? thx in advance!

Are you an insider? Because unless you are FDA or with Mannkind, you would not have access to say “yet when I review the inspections performed by the FDA at that facility.”

Also, when the company pr’s that FDA has questions with storage process, this is part of manufacturing. This has occurred 2 times now, which indicates there could be a problem.

My premise with Mannkind is that I do not trust them. They engage in excessive and often time misleading promotion. Now, do you mean you read what Mannkind said about the inspections?

No, not an insider. I just looked at the FDA inspection database which is available to everyone and in there it shows MNKD was inspected 3 times, twice in 2009 and once in 2013. It’s not updated yet to reflect if MNKD was inspected in 2014 past march. Two inspections were labeled as VAI which, as you probably know, occurs when objectionable conditions or practices were found that do not meet the threshold of regulatory significance. Inspections classified with VAI violations are typically more technical

violations of the FDCA.

What I don’t know is if the facility was inspected since march 2014 and what the results of that inspection might be since that information isn’t public on the database as of yet.

oh, and the clarify, I misstated in my original post when I said they had 3 NAI’s…..in fact, it was indicated on the database that one inspection as NAI (no issues) and two of the inspections were listed as VAI, which I assume is related to what you’re speaking about.

I too have reservations about how MNKD disseminates information including their recent comments during the big 3 presentations where they are outlining timelines for a possible partnership. Very, very thin ice there and, imho, not what I would expect from a company in MNKD’s position at this stage of the game.

I do, however, believe the FDA will approve but I don’t believe the label will be favorable, much like vvus as an example. As a result, any partnership that does materialize will reflect the labeling limitations and won’t be nearly as lucrative as many seem to believe. On top of that, partnership agreements, while lucrative, are likely to have percentage of rev split between the two and that means MNKD will be at the short end of the percentage. Point is, rev’s are going to be much lower. Example – if the partner sells 1 billion worth of product, MNKD will see 300 million. Again, just an example. IN that example, MNKD can claim blockbuster status but their bottom line won’t look like it. Will take years in that scenario to develop into a money making product for MNKD, if ever. Anyway, just some thoughts and thanks for your response.

I pretty much feel the same way David. My view is more based on the company constantly mis guiding, misleading, it goes to trust. The FDA is not too keen on Al Mann, and might look for a reason to CRL. However, I do agree, that if approved, the label will be very restricted, and I believe any partner would be a standard 10% or so, with possible tier royalties. Also, does big pharma really want to touch this one as they got burned on Exhubera? While different type of Insulin, still insulin, and drop out rate was high, patients developed nasty coughs, and 3 somehow ended up with cancer.

Personally, I think the adcom was wrong, and it might be the FDA catches it. Regardless, after some time, I expect Mannkind stock to head back to the @3 range or so. thanks for the comments, I appreciate intelligent discussion!